I’m 72 and Own My Home Outright, I Almost Signed a Reverse Mortgage Until I Found This Instead

“Meet Joan, a retired teacher from Arizona who found a safer, smarter alternative to a reverse mortgage. She finally got the financial peace of mind she’d been looking for.”

Hi, I’m Joan and I Was This Close to Doing a Reverse Mortgage

I’m 72, retired, and have lived in the same home for over 30 years. It’s nothing fancy, but it’s mine. No mortgage, just a lot of memories, a little yard for my dog, and some creaky floorboards I’ve grown to love.

But like a lot of folks my age, retirement costs more than I expected. Between rising groceries, medical bills, and helping my grandson with college, my savings were thinning out fast.

So I started looking for options. That’s when the reverse mortgage ads started showing up on TV, in the mail, even my email.

They Make Reverse Mortgages Sound So Easy

“Use the equity in your home!”

“No payments ever!”

“Stay in your house for life!”

I thought, Why not? I wasn’t trying to live large, I just wanted to cover a few things and breathe a little easier.

So I called one of those companies.

Here’s What They Didn’t Mention in Their Reverse Mortgage Ads

The nice man on the phone gave me the basics, but when I read the documents… I got a pit in my stomach.

- There were thousands in upfront fees.

- My loan balance would grow every month, even if I didn’t touch the money.

- If I didn’t keep up with property taxes or maintenance, I could lose the house.

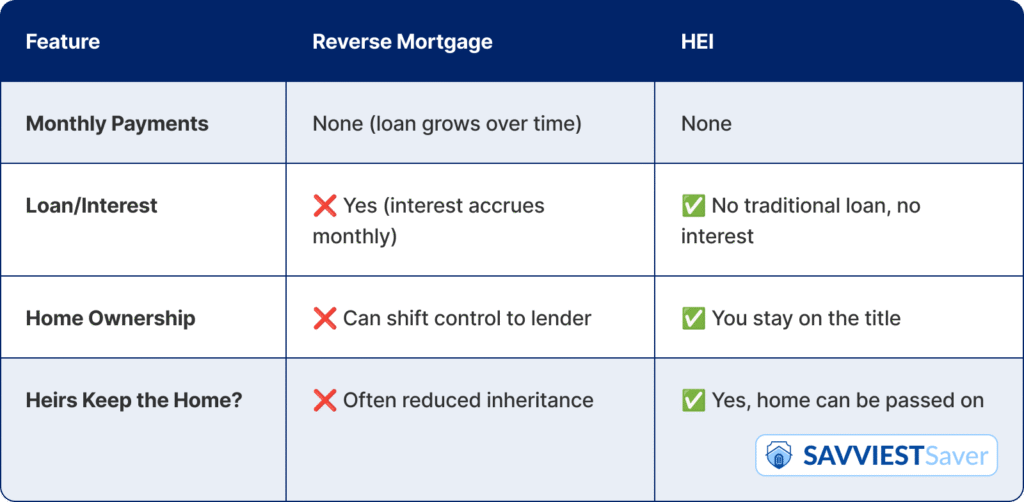

- And when I passed, my daughter might not inherit the home at all, just whatever was left after the lender took their share.

I didn’t like the idea of giving up control of the one thing I’d worked my whole life for…so I paused and tried to find a different option.

That’s When I Found Point.com

A friend from church mentioned something called Point, a way to access cash from your home without taking out a loan.

At first, I didn’t get it. No payments? No loan? What’s the catch?

But I called them, and the woman I spoke with actually took the time to explain everything clearly.

Here’s What I Learned (and Why I Said “Yes”)

Point offers something called a Home Equity Investment (HEI). With an HEI, there are no monthly payments or interest rate. You’re simply unlocking your equity in exchange for a share of your home’s future value on your terms.

✅ No interest charges.

✅ No monthly payments.

The best part? I stay on the title. I keep the house. And I can pass it on.

Quick Comparison Between Point and a Reverse Mortgage:

What I Used the Money For

I didn’t splurge. I…

- Paid off a lingering medical bill

- Helped my grandson with tuition

- Fixed the AC before summer (thank goodness)

- Set some aside (just to feel safer)

It gave me breathing room, not just financially, but emotionally.

If You’re Over 60 and Own a Home, Read This

Reverse mortgages aren’t evil, but they’re not for everyone. I almost signed without realizing how much I’d be giving up.

With Point, I didn’t feel rushed. I didn’t feel tricked. I felt like someone actually looked at my situation and said, Let’s find something that works for you.

If you’re sitting on home equity, but don’t want debt or drama, I really recommend you look into Point. Not everyone will qualify, but many will.

No pressure. Just honest options. It’s free to check →

Terms and conditions apply. Some applicants will not qualify. Not available in all states.