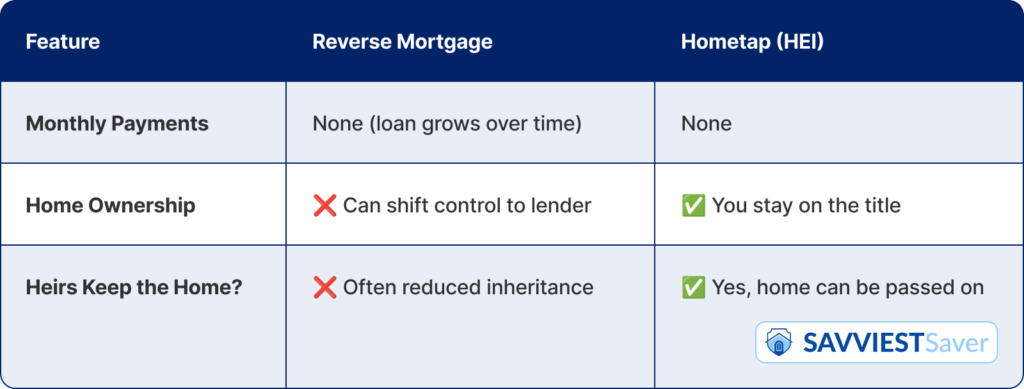

Hometap offers something called a Home Equity Investment (HEI). You receive a lump sum of money now in exchange for a share of your home’s future value when you sell or refinance down the line.

No monthly payments. No risk of foreclosure if you fall behind on taxes. And the fees? A fraction of what the reverse mortgage company quoted me.

No monthly payments. No risk of foreclosure if you fall behind on taxes. And the fees? A fraction of what the reverse mortgage company quoted me.

The best part? I stay on the title. I keep the house. And I can pass it on.

Quick Comparison: